That reverse mortgage scheme the government is about to re-announce, how does it work?

- Written by Colin Zhang, Lecturer, Department of Actuarial Studies and Business Analytics, Macquarie University

Many Australians have never heard of the Pension Loans Scheme, and many more assume it’s just for pensioners, which is understandable given its name.

That’s why the government is poised to rename it the Home Equity Access Scheme and make the interest rate it charges more reasonable, in the mid-year budget update on Thursday.

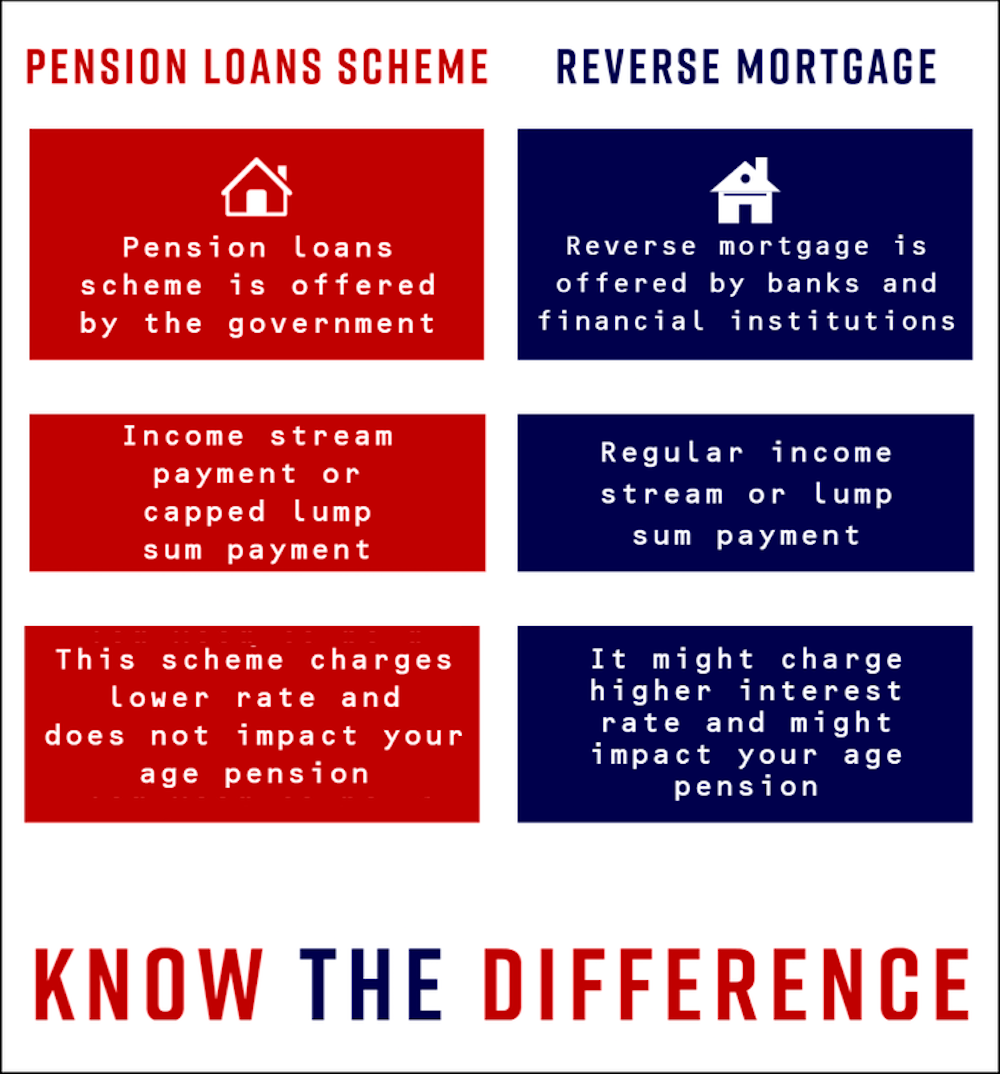

The soon to be renamed scheme is best thought of as a reverse mortgage where instead of paying down a home loan each month, the homeowner borrows more against the home each month, paying off what’s borrowed when the home is eventually sold.

Although reverse mortgages have been provided commercially for some time, the number of providers has shrunk as large banks have left the field in the face of increased scrutiny and compliance costs.

The government version is misleadingly named the Pension Loans Scheme (PLS), even though it is available to all retirees with homes and not just pensioners. It was introduced by the Hawke government in 1985.

The maximum amount that can be made available under the scheme and the age pension combined is 150% of the full pension. This means a retiree who is on the pension can get extra fortnightly payments from the scheme to bring their total payment up to 150% of the full pension.

If the retiree is not on the pension they can get the entire amount of 150% of the pension via the PLS.

Read more: Is it worth selling my house if I'm going into aged care?

The payments stop when the loan balance reaches a ceiling which climbs each year the retiree gets older and climbs with increases in the value of the home.

The ceiling for a 70-year old with a home worth $1,000,000 is $308,000.

The key difference between the PLS and commercial reverse mortgages is that the size of its lump sum payments is limited. Payments under the PLS have no impact on the pension, whereas commercial reverse mortgages can trigger the means test.