How do we protect students from ballooning HELP debts? A fixed maximum indexation rate would help

- Written by Andrew Norton, Professor in the Practice of Higher Education Policy, Australian National University

The indexation of student debt is arguably the federal government’s biggest political problem when it comes to universities.

Last June, student debt balances increased by 7.1%, the highest rate in decades. While HELP loans do not attract interest, they are indexed to inflation as measured by the Consumer Price Index (CPI).

When inflation remained low, this was not an issue for those with a HELP debt. But last year, as inflation rose, on average A$1,700 was added to each borrower’s debt. The next indexation date is approaching on June 1. We won’t know the 2024 indexation rate until the March quarter CPI level is released, but it’s likely to be around 5%.

Calls for change

At the same time, community pressure is building.

An online petition started by independent MP Monique Ryan is calling for a change to the way debts are indexed. It has amassed more than 230,000 signatures. Other independent, Greens, Liberal and backbench Labor MPs are also raising the issue in federal parliament.

Media reports regularly highlight the stress students and graduates experience due to their rising debts.

So what should happen?

In February, the Universities Accord final report proposed setting indexation at the lower of CPI or the Wage Price Index (WPI), which measures wage increases.

The government is now “looking at” this recommendation (along with all the others in the report). But it should be considering an alternative.

While the WPI would have lowered indexation in recent years, in most years it is higher than CPI. This means students would not necessarily be better off.

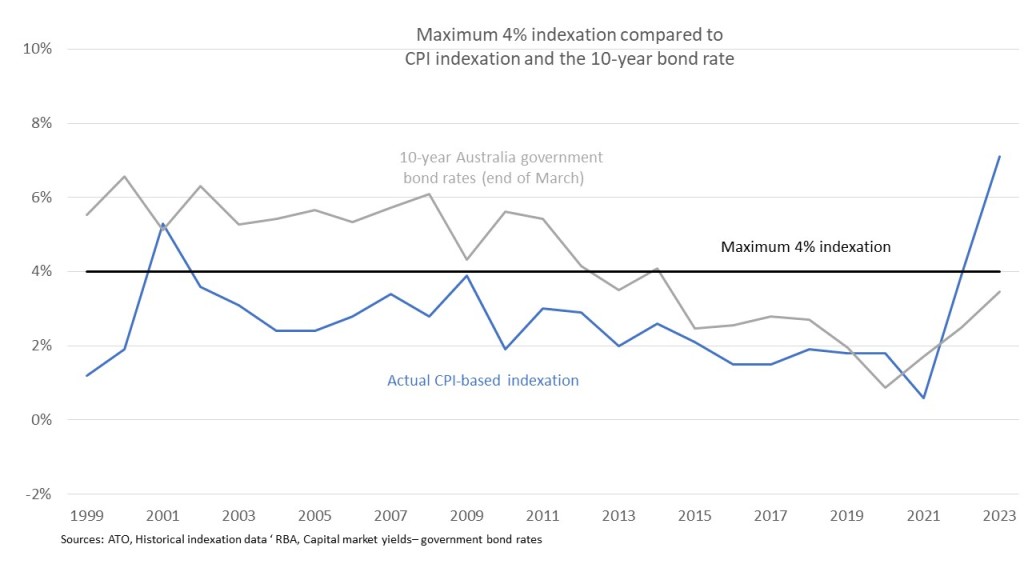

This is why a fixed maximum indexation rate of 4% would better protect HELP borrowers against unpredictable increases in their student debt.

Read more: Universities Accord: many students could pay less for their higher education ... eventually

A lower-of two indicators indexation system

The accord’s proposed “lower-of two” indicators indexation policy aims to balance competing policy considerations: the cost to government of lending to students and minimising the risk to borrowers of unexpected spikes in their debt.

As of June 30 2023, current and former student borrowers owed $78 billion. Due to the government’s own large debt, it pays significant interest on the student component, which explains why it has not rushed to change indexation policy.

Any economic indicator-based indexation system risks years of high indexation. Using CPI, average indexation between 2000 and 2021 was 2.5%, in line with a strong policy commitment to keep inflation in the 2% to 3% range. But the unusual economic conditions caused by COVID triggered an inflationary spike, flowing through to 3.9% indexation in 2022, 7.1% in 2023 and probably around 5% this year.

This has raised the question of what alternative indicators we could use to index student debts. Suggestions include the government bond rate and measures of wage increases.

The government bond rate

Of these options, the government bond rate makes policy sense if we consider both sides of the transaction. The bond rate is the interest rate the government pays when it borrows money. So it is directly relevant to the cost indexation offsets, which is public debt interest on outstanding student loans.

In most years, CPI is less than the bond rate, so indexation only partly covers the government’s costs. But unusually, CPI indexation exceeded the ten-year bond rate in three of the last four years.

So, the government has made a profit on indexation, which is not a policy goal. Past proposals for “real” interest on student debt (inflation plus a margin), have always failed to secure parliamentary support. Real interest would cost all HELP debtors more than the usual CPI indexation of about 2.5%. So this is a difficult policy to sell politically, as the last two years have shown.

Wage growth indexation

The accord final report preferred a wage measure to the bond rate for indexing student debts.

WPI measures increases in hourly pay rates for the same job. The accord report’s logic is that weak wage growth in recent years undermined the long-term capacity of student debtors to repay. So WPI would maintain a relationship between earnings and debt.

A lower-of either CPI or WPI formula, however, would not reliably save HELP debtors money. WPI has been below inflation indexation levels just four times in the last 25 years. Two of these four are the high indexation years of 2022 and 2023, but these do not reflect the normal relationship between the two indexes.

WPI is usually higher than CPI because workers seek inflation-compensation wage rises plus real wage increases. The COVID lockdown period suppressed both CPI and wage levels. Wages took time to catch up after sudden inflation during the post-lockdown economic recovery. The latest wages figures show they are now again above inflation

Authors: Andrew Norton, Professor in the Practice of Higher Education Policy, Australian National University

{kind=link}